Statistics in Miami-Dade and Broward june 2024/2025

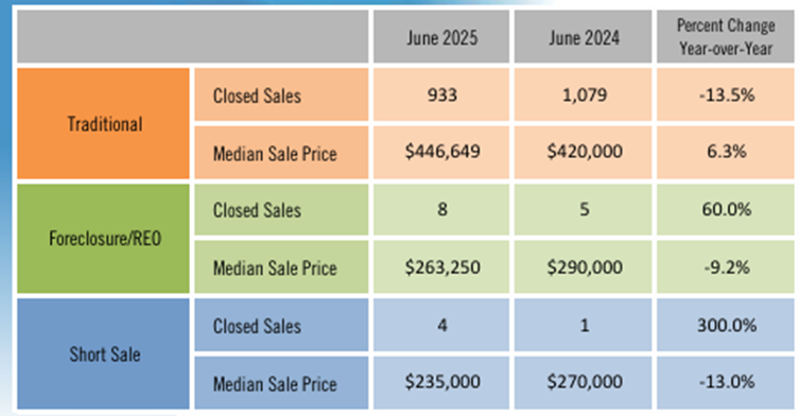

Monthly Market Summary- JUNE 2025 Single-Family Homes Miami-Dade County

CONCLUSION

The Miami-Dade real estate market in June 2025 shows signs of adjustment and moderate cooling; although median prices continue to rise, the pace of sales is slowing; there is more inventory available, and buyers are taking longer to finalize real estate closings; therefore, buyers have a good opportunity to find more advantageous strategies and deals.

INFORMATION AND ANALYSIS

Closed sales decreased by 14.4%, indicating a slowdown in purchase activity. Even more significant is the 23.9% drop in cash, suggesting less participation from investors or buyers without financing.

Despite less activity, prices continue to grow by 3.8%.

Dollar volume fell 17.5%, reflecting a lower number of transactions.

The sales process has been slower, considering an increase in the average time for each contract by 21.2% and the average time to close by 2.6%.

Inventory offered in the active market increased sharply by 44.0%, with more properties available, thus favoring buyers.

An upcoming slowdown is forecast due to the 134.6% drop in pending sales and a 16.7% drop in pending inventory.

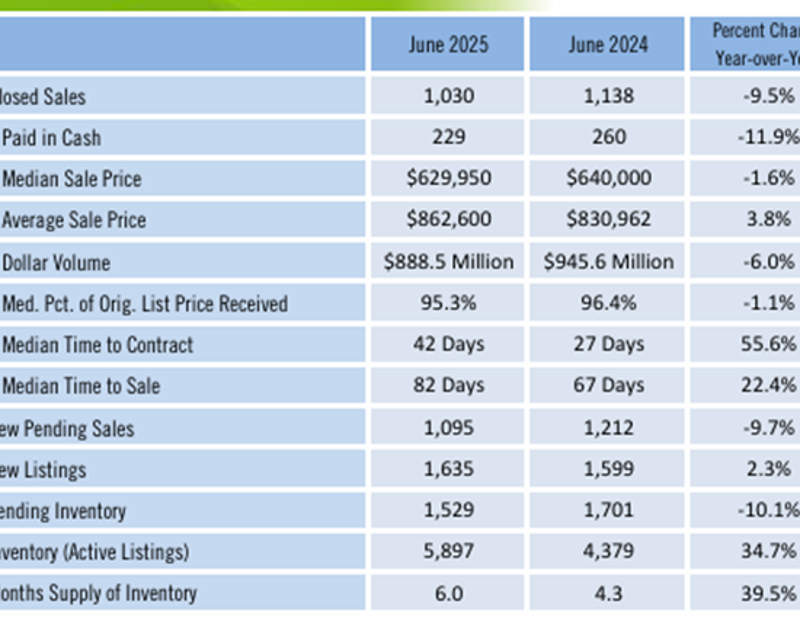

Monthly Market Summary- June 2025 Townhouses and Condo Miami-Dade County

CONCLUSION

The market is leaning towards an adjustment due to the cooling caused by the decrease in sales, although prices have slightly increased and require more time on the market, which translates into an advantage for buyers in the negotiation of prices and conditions.

INFORMATION AND ANALYSIS

In the townhouses sector, sales and transaction volume fell 12.9%, with a 13.8% decrease in sales volume. Prices were forecast to rise by 6.0%, with a 1.1% drop, reflecting relative stability within the market range.

Time to close increased by 36%, and time to close increased by 18.9%, indicating slower closing times.

Pending inventory fell by 15.2%, and active listings grew by 36.1%, suggesting an increased inventory supply of 58.4%, signaling a buyer-friendly market.

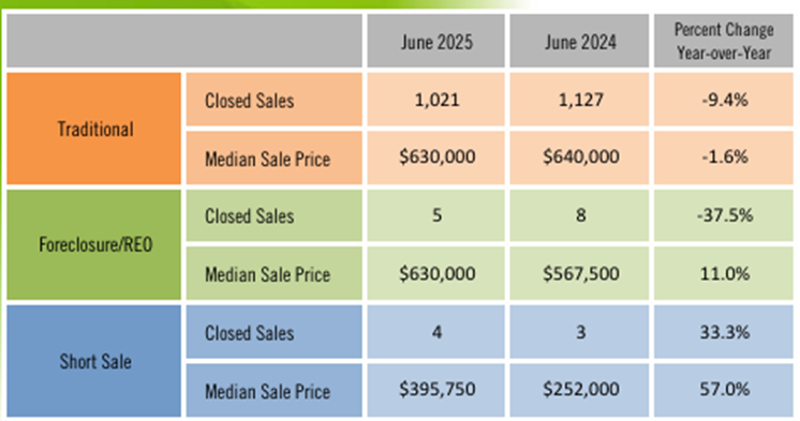

Monthly Market Summary- June 2025 Single-Family Homes Broward County

CONCLUSION

This market is showing signs of slowing, with fewer sales and more inventory, with longer closing times. Although the average price increased, the median price decreased slightly, indicating that more high-value properties are selling, but with lower overall volume. This is a favorable scenario for analytical buyers and a warning for sellers who should consider further adjustments and strategies.

INFORMATION AND ANALYSIS

In Broward, single-family closed sales fell 9.5%, along with a 6.0% drop in total sales volume.

The median price fell slightly by 6.0%, but the average price increased by 3.8%, indicating an increase in sales of higher-value properties.

The median time to sign a contract lengthened by 55%, and the total time to sell increased by 22.4%, reflecting a more relaxed market.

The market is leaning toward more inventory and less demand, with pending new sales down 9.7% and pending inventory falling 10.1%, reflecting less immediate buying pressure.

Active properties in inventory increased 34.7%, and the monthly inventory supply grew 39.5%, with a slight difference in time of approximately two months, indicating a balanced market.

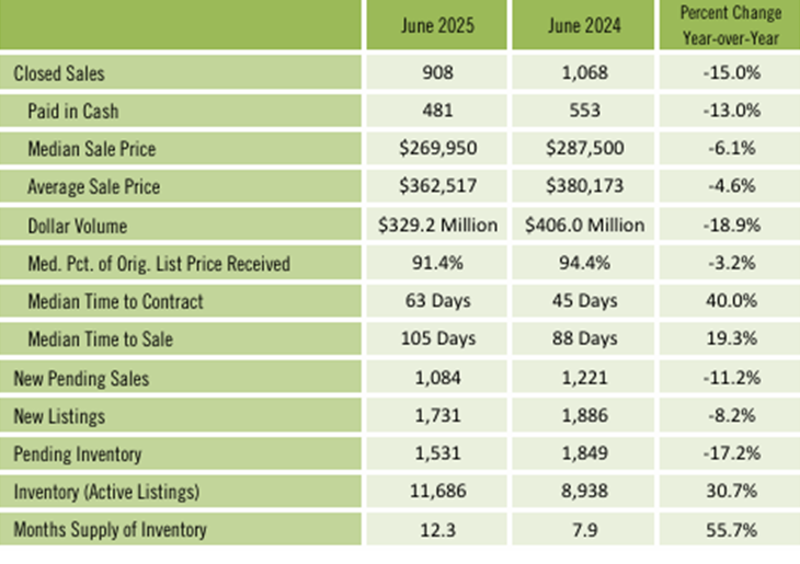

Monthly Market Summary- June 2025 Townhouses and Condo Broward County

CONCLUSION

This market is showing a clear cooling, with fewer sales, resting prices, more time to close, and a significant increase in inventory. This represents an opportunity for buyers to negotiate and a warning for sellers who must adapt to new strategies.

INFORMATION AND ANALYSIS

Here we have lower closed sales activity, which fell by 15%. Total dollar volume fell 18.9%, reflecting fewer transactions and lower prices.

The median sales price fell 6.1%, and the average sales price also fell 4.6%, suggesting greater downward pressure in the market, with more properties selling below their 2024 value.

Requiring longer time to close: the median time to contract increased 40.0%, and the total time to sell increased 19.3%, indicating a slower market and longer negotiations.

The market is leaning toward lower future demand and higher inventory, with pending sales decreasing by 11.2% and pending inventory decreasing by 17.2%, indicating a slower closing pace.

Active properties in inventory increased by 30.7%, and the monthly inventory supply increased 55.7%, clearly moving closer to a more favorable market for buyers.